Chapter 6: Employer Payroll Expenses

6.2 Employer CPP Contributions and EI Premiums

Employers are required by law to contribute to the Canada pension plan (CPP) and employment insurance (EI). Contribution rates vary annually, and employer contributions are set at a fixed ratio to employee contributions. In other words, to calculate employer contributions, employee calculations are multiplied by a certain percentage.

6.2.1 Canada Pension Plan (CPP) Contributions

Employers must match employees’ CPP contributions one-to-one. If an employee pays $1,000 annually in CPP contributions, the employer would also pay $1,000 for that employee. Each employee’s contribution is matched by the employer and remitted to the CRA. CPP contribution rates can be found online: Calculate CPP contributions and deductions

Employers must match employees’ CPP contributions one-to-one. If an employee pays $1,000 annually in CPP contributions, the employer would also pay $1,000 for that employee. Each employee’s contribution is matched by the employer and remitted to the CRA. CPP contribution rates can be found online: Calculate CPP contributions and deductions

Detailed information about how to calculate the employee’s CPP contribution can be found in Chapter 4.2 Source Deductions. Note that if the employee contributes to CPP2, the employer must also match this amount.

Employers do not have to make CPP contributions for independent contractors. Self-employed individuals make both the employer and employee contributions (Government of Canada, 2021a). Anyone with self-employment income can choose to file an election to stop contributing to CPP on their self-employment income by completing a Schedule 8 form.

6.2.2 Employment Insurance (EI) Premiums

Employer EI premiums are calculated as 1.4 times the employee premium. EI rates can be found here: EI premium rates and maximum

Employer EI premiums are calculated as 1.4 times the employee premium. EI rates can be found here: EI premium rates and maximum

For detailed information about how to calculate employee EI premiums, see Chapter 4.3 Employment Insurance.

Employers can make a written request to Service Canada to reduce the employer contribution factor for all employees; if employers qualify, the employer contribution would be reduced to an amount less than 1.4 times the employee contributions. To qualify for a reduction, the employer must provide a short-term disability plan deemed acceptable by the CRA (Government of Canada, 2023b). Once an employer is granted an EI reduction, that reduction remains in place until or unless the employer changes or cancels their short-term disability plan (Government of Canada, 2021b).

For the employer, the logic behind this reduction is that by providing a plan that covers employees’ short-term disability, the employer can potentially lower the employer-side EI expense. For the Canadian government, when employers provide their employees with a paid short-term disability leave, those employees are able to use that short-term disability leave instead of EI, reducing the government’s EI payouts.

6.2.3 Using the CRA Payroll Deductions Online Calculator (PDOC)

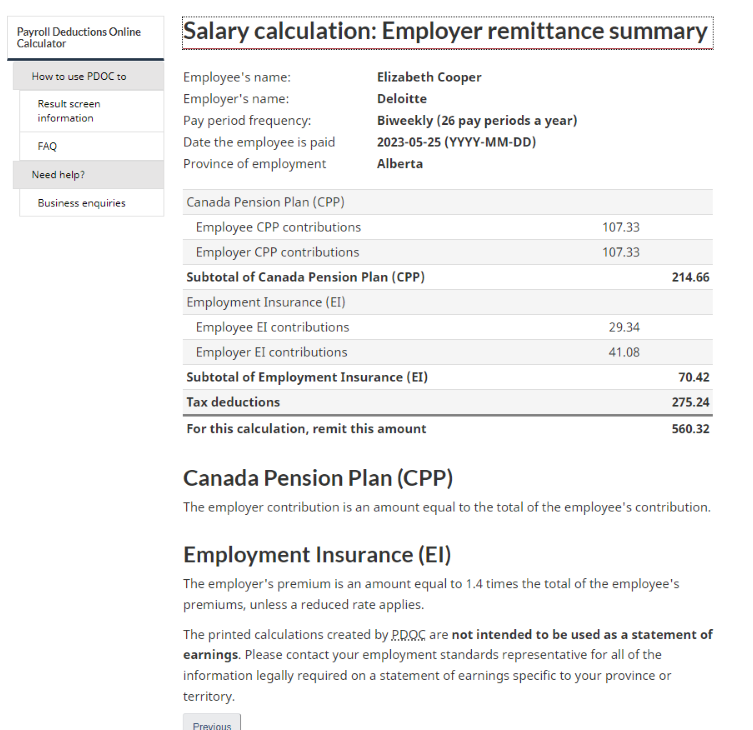

If the CRA’s Payroll Deductions Online Calculator (PDOC) is used to determine payroll deductions (see Chapter 4), the PDOC can generate an employer remittance summary, including the employer portions of EI and CPP.

When the calculation is complete, the option to click on Employer Remittance Summary can be found at the bottom of the page.

The employer remittance summary lists employer and employee CPP contributions and EI premiums, and the subtotals of each.

References

Government of Canada. (2024a). 5000-S8 Schedule 8 – Canada Pension Plan contributions and overpayment (for all except QC). https://www.canada.ca/en/revenue-agency/services/forms-publications/tax-packages-years/general-income-tax-benefit-package/5000-s8.html

Government of Canada. (2024b). Calculate payroll deductions and contributions: EI premium rates and maximums. https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/payroll/payroll-deductions-contributions/employment-insurance-ei/ei-premium-rates-maximums.html

Government of Canada. (2024c). How to calculate: Calculate CPP contributions and deductions. https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/payroll/payroll-deductions-contributions/canada-pension-plan-cpp/cpp-contribution-rates-maximums.html

Government of Canada. (2024d). Line 22200 – Deduction for CPP or QPP contributions on self-employment income and other earnings. https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/about-your-tax-return/tax-return/completing-a-tax-return/deductions-credits-expenses/line-22200-deduction-cpp-qpp-contributions-on-self-employment-other-earnings.html

Government of Canada. (2024e). Payroll deductions online calculator. https://www.canada.ca/en/revenue-agency/services/e-services/digital-services-businesses/payroll-deductions-online-calculator.html

Government of Canada. (2023a). Calculate payroll deductions and contributions: CPP contribution rates, maximums and exemptions. https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/payroll/payroll-deductions-contributions/canada-pension-plan-cpp/cpp-contribution-rates-maximums-exemptions.html

Government of Canada. (2023b). EI premium reduction guide Chapter 1: General information about the Employment Insurance premium reduction. https://www.canada.ca/en/employment-social-development/programs/ei/ei-list/reports/reduction-program/general.html

Government of Canada. (2023c). EI premium reduction program: For employers. Employment and Social Development Canada. https://www.canada.ca/en/employment-social-development/programs/ei/ei-list/ei-employers/premium-reduction-program.html

Government of Canada. (2021a). Contributions to the Canada Pension Plan. https://www.canada.ca/en/services/benefits/publicpensions/cpp/contributions.html

Government of Canada. (2021b). EI premium reduction guide Chapter 6: Changes that may affect your premium reduction. https://www.canada.ca/en/employment-social-development/programs/ei/ei-list/reports/reduction-program/changes.html

Image Credits (images are listed in order of appearance)

Government of Canada. (2024a). Salary calculation: Result [Screenshot]. https://apps.cra-arc.gc.ca/ebci/rhpd/beta/results

Government of Canada. (2024b). Salary calculation: Employer remittance summary [Screenshot]. https://apps.cra-arc.gc.ca/ebci/rhpd/beta/payrolldeductionsremittancesummary